Carbon transparency in practice: how to approach CDP in 2026

CDP (Carbon Disclosure Project) reporting is no longer the domain of only the largest corporations. In the past year alone, more than 23,000 companies worldwide used it, collectively representing nearly two-thirds of global market capitalization. The reason is simple: investors, customers, and other stakeholders are increasingly monitoring how companies approach environmental risks and opportunities. CDP provides a transparent tool that allows them to do so easily and in one place.

At the same time, it doesn’t have to be only about external pressure on companies. A CDP report also helps organizations better understand their own carbon footprint, set meaningful targets, and communicate them more effectively with partners.

Author: Richard Fleischhans

Our experience

CI3, s.r.o. still holds the title of the only accredited CDP partner for the Czech Republic and Slovakia. We have been supporting CDP reporting itself for six years, and we have more than a decade of experience in carbon footprint calculation. We are certainly not newcomers in this field, and we are glad this is also one of the reasons clients regularly turn to us.

The Czech and Slovak companies we supported in completing their CDP reports last year achieved the highest ranking levels, all reaching at least a B rating. We know not only how to correctly complete the questionnaire, but also how to get the most value out of it—whether you are just starting with CDP or filling it out for the second or third time.

What to expect from the questionnaire

The CDP questionnaire consists of several sections: an introductory company profile, governance and management approach, risk and opportunity analysis, business strategy, value chain engagement, and reporting on carbon footprint, energy consumption, and decarbonization targets, followed by a final section.

Companies with fewer than 1,000 employees and annual revenue below 200 million USD can use a simplified version of the questionnaire. It covers all key areas, just in a more accessible format. This means that even smaller companies have a fully viable opportunity to participate.

CDP questionnaires cover multiple environmental areas—meaning all the sections mentioned can be completed from the perspective of climate change, water, and “forests” (which includes agricultural commodities, timber, coffee, rubber). Each of these perspectives has its own separate scoring. Which one you are expected to report on is determined either by your materiality assessment, CDP requirements (some sectors have certain themes pre-defined as material), or by the requirements of your business partner requesting the CDP disclosure.

Within CDP reporting, three types of companies can be distinguished.

The first group consists of companies that have been asked by one of their customers to complete the CDP questionnaire.

The carbon footprint of suppliers feeds into the indirect (Scope 3) emissions of their customers, while at the same time customers are exposed to climate-related risks within their supply chains. Large companies therefore often cooperate with CDP and require their suppliers to complete the questionnaire. The requesting company then gains access to the suppliers’ responses and results, allowing them to better manage or respond to climate risks and track emissions developments across their supply chain. The advantage for suppliers is that they do not have to pay to complete the questionnaire. Around 270 large companies cooperate with CDP in this way (e.g. Microsoft, L’Oréal, Walmart).

The second group includes large companies—often those active on financial markets—that are requested by “the market” to complete the CDP questionnaire.

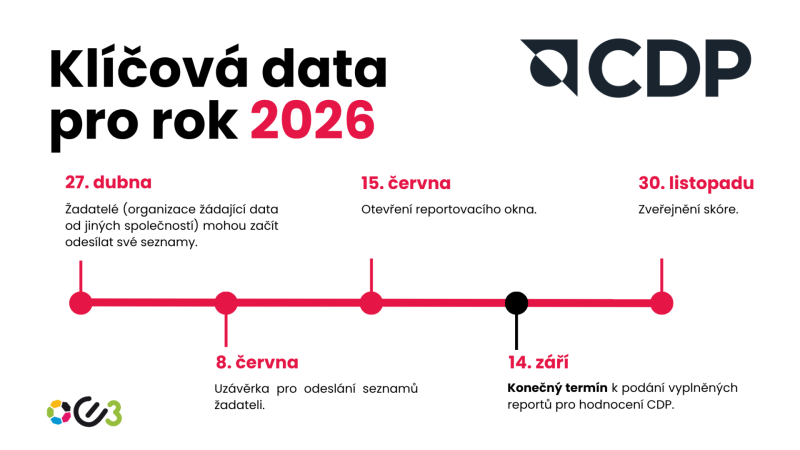

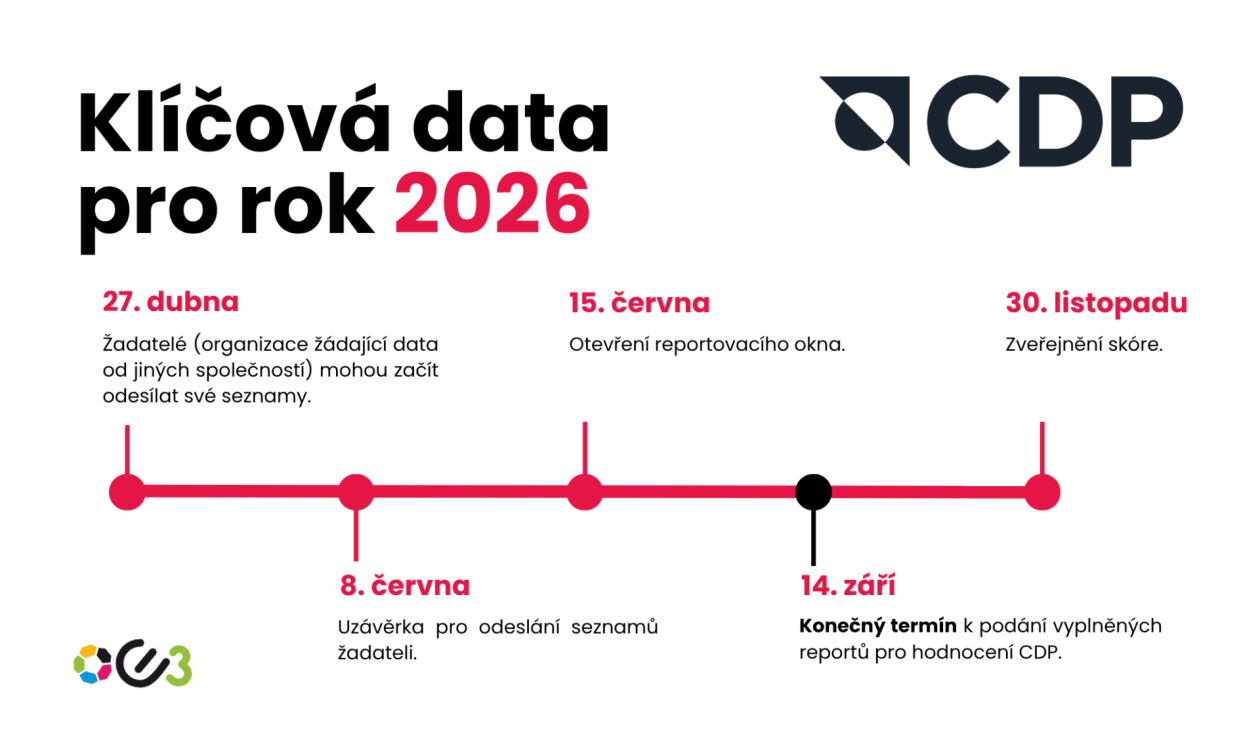

CDP works with approximately 600 financial institutions, which each spring submit lists of companies they would like to see respond to the CDP questionnaire.

The list is anonymized, so it is not possible to see which specific institution has requested the disclosure. Companies should be informed of this request by CDP, but in practice this does not always work reliably. The list of companies that have been approached is public. If a company does not respond and does not participate in CDP reporting, it will not be scored. If it does participate, it must pay for access to the questionnaire (with a base fee of around 3,000 EUR), and its results and responses are then shared with the financial institutions, which typically use them for internal assessments.

The final—but no less important—group consists of voluntary participants.

CDP has a strong reputation, and achieving a good score already carries weight, as shown by the growing number of participating companies and financial institutions involved. Although participation is voluntary, these companies also pay for access to the questionnaire under the same conditions as market-requested entities. Participation is often seen as an opportunity to increase visibility and demonstrate that the company is preparing for future climate-related impacts and the expected transition away from fossil-fuel-based technologies.

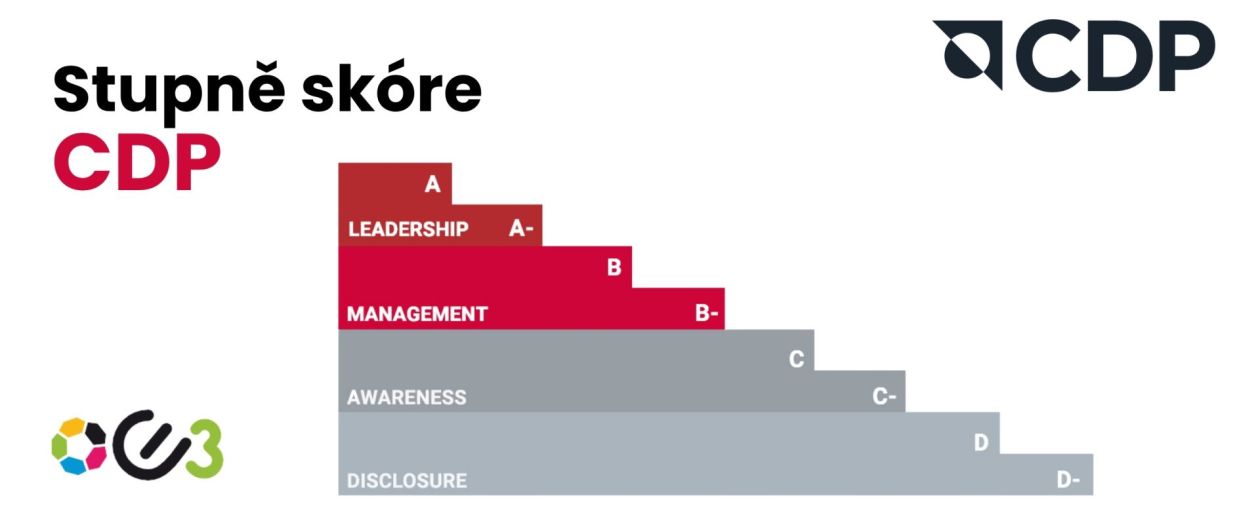

Scoring within Climate Change

CDP scoring is relatively strict. It is based on four levels: disclosure (D score), awareness (C score), management (B score), and leadership (A score). Based on our experience with CDP reporting, the typical state of companies achieving each score can be described as follows:

Disclosure score (D score)

The company is able to complete most basic data fields. It either does not have a defined carbon footprint or only a partial one. There is no established carbon management system and no initiatives in place to reduce greenhouse gas emissions. However, achieving a D score (not D-) means the company has responsibly completed the questionnaire.

Awareness score (C score)

The company has a basic overview of its carbon footprint and is able to describe it. It has partially established processes or is in the early stages of setting them up for future carbon management. In its risk analysis, it begins to consider risks related to climate change.

Management score (B score)

The company has well-established processes for both carbon footprint calculation and its management. Top management is actively involved in decision-making and regularly evaluates emissions development. Climate-related risks and dependencies are fully integrated into risk analysis. The company also looks beyond its own operations, assessing suppliers and value chain risks. It can identify opportunities such as cost savings or new low-carbon products. The company has set sufficient emission reduction targets and is actively working on them.

Leadership score (A score)

The company has a carbon footprint verified by an independent auditor, or its entire sustainability report is externally verified. Climate change is a standard agenda item at board level. The company has ambitious emission reduction targets and a defined transition plan, and management compensation is linked to these targets. A significant share of its energy comes from renewable sources, and the company continuously implements measures to reduce emissions. It works closely with both suppliers and customers, requiring them not only to report emissions but also to demonstrate how they plan to reduce them in the future.

Sources:

CDP – Supply Chain: https://www.cdp.net/en/supply-chain

CDP – Capital Markets Signatories: https://www.cdp.net/en/capital-markets-signatories

CDP – Framework Alignment: https://www.cdp.net/en/about/framework-alignment

CDP – Disclosure 2026: https://www.cdp.net/en/disclosure-2026

GHG Protocol: https://ghgprotocol.org/

IFRS – IFRS S2 Climate-related Disclosures: https://www.ifrs.org/issued-standards/ifrs-sustainability-standards-navigator/ifrs-s2-climate-related-disclosures/

TCFD Recommendations: https://www.fsb-tcfd.org/recommendations/

GRI Standards: https://www.globalreporting.org/standards/

TNFD: https://tnfd.global/